Payday Loan vs Installment Loan: Which Is Better for You?

When you need fast cash, two common options are payday loans and installment loans. Both can provide quick funding, but they differ dramatically in cost, repayment structure, credit requirements, and risk. Choosing the wrong option can trap you in debt or cost you thousands in unnecessary fees. This guide breaks down every difference so you can make an informed decision.

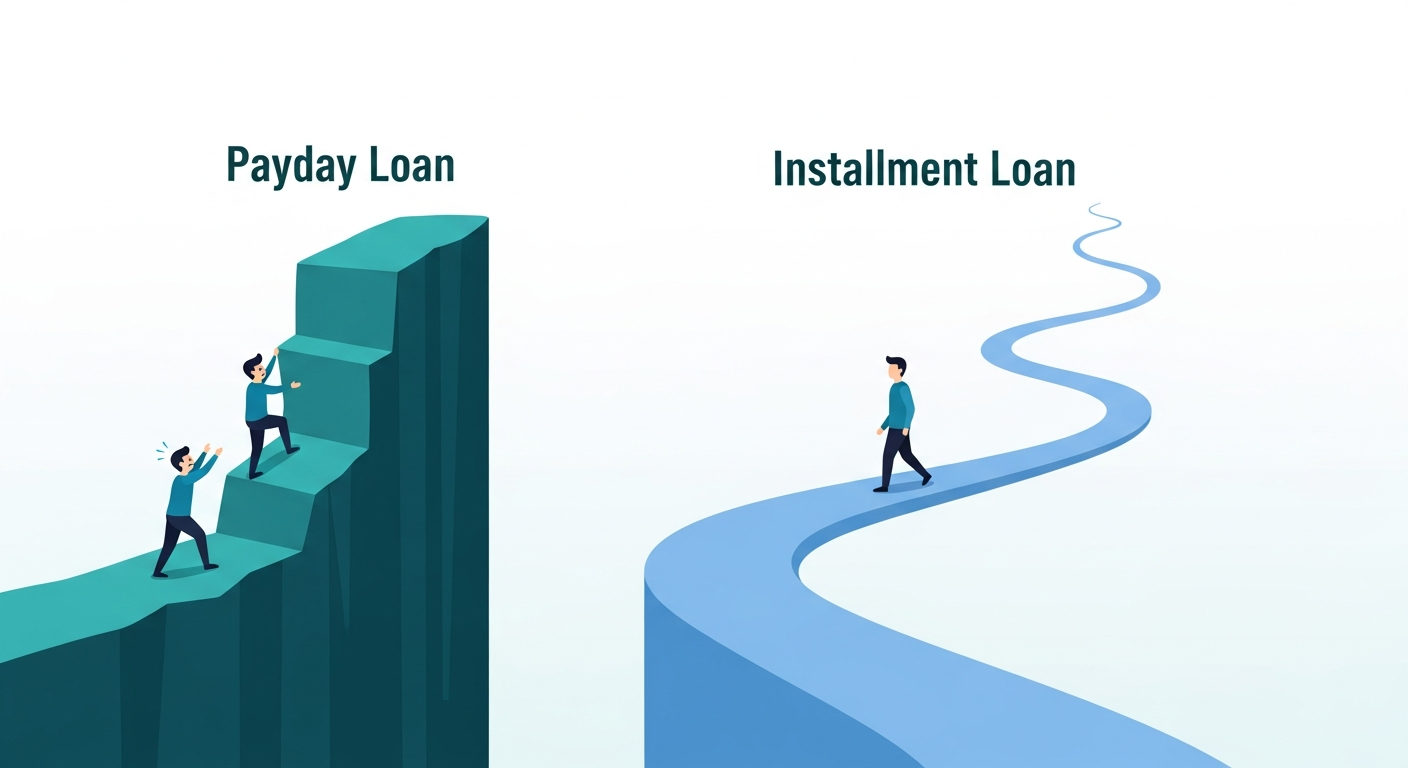

What Is a Payday Loan?

A payday loan is a short-term, high-cost loan typically due on your next payday — usually 2–4 weeks after borrowing. You provide a post-dated check or bank account authorization, and the lender withdraws the full amount (principal + fees) on the due date. Key characteristics:

- Amount: $100–$1,500 (average $375)

- Term: 2–4 weeks

- APR: 300–600% (national average 391%)

- Fee: $15–$30 per $100 borrowed

- Credit check: Minimal or none (soft pull only)

- Repayment: Single lump-sum payment

Payday loans are designed for emergencies when you have no other options and are certain you can repay on the due date. The single-payment structure is the biggest risk — if you cannot repay in full, you must roll over the loan, which triggers new fees and compounds the debt.

What Is an Installment Loan?

An installment loan is a longer-term loan repaid in fixed monthly payments (installments) over 3–60 months. You can borrow larger amounts, and the extended term makes payments more manageable. Key characteristics:

- Amount: $500–$50,000 (average $3,000)

- Term: 3 months to 5 years

- APR: 6–36% (average 18–25%)

- Fee: Origination fee of 1–8% (deducted from loan amount)

- Credit check: Required (hard pull), but bad-credit options exist (APR 25–36%)

- Repayment: Fixed monthly payments

Installment loans are better for larger expenses, debt consolidation, or when you need more time to repay. The structured repayment schedule makes budgeting easier, but the credit check and longer commitment may not suit everyone.

Side-by-Side Comparison

| Feature | Payday Loan | Installment Loan |

|---|---|---|

| Loan amount | $100–$1,500 | $500–$50,000 |

| Repayment term | 2–4 weeks | 3–60 months |

| APR | 300–600% | 6–36% |

| Total cost for $1,000 | $150–$300 in fees | $60–$180 in interest |

| Credit check | Minimal/none | Hard pull required |

| Funding speed | Same day (1–24 hours) | 1–3 business days |

| Impact on credit | Usually not reported (unless default) | Reported to all 3 bureaus (helps build credit) |

| Risk of debt trap | High (rollover fees add up) | Low (fixed payments, no rollovers) |

When to Choose a Payday Loan

A payday loan may be the better choice in these limited situations:

- True emergency: You need cash within hours for a medical emergency, car repair, or utility shut-off.

- Small amount: You need $200–$500 and can repay in full on your next payday.

- No credit check needed: Your credit score is below 500 and you have been rejected for other loans.

- Short-term bridge: You have guaranteed income arriving in 1–2 weeks and just need to bridge the gap.

Even in these situations, cash advance apps like Dave, Earnin, or Brigit are often cheaper and safer than payday loans. Consider them first.

When to Choose an Installment Loan

An installment loan is usually the better choice for:

- Debt consolidation: You have multiple payday loans and want to combine them into one lower-APR loan with fixed monthly payments.

- Larger expenses: You need $1,000+ for a car repair, medical bill, or home fix.

- Credit building: You want to improve your credit score by making on-time payments that are reported to credit bureaus.

- More time to repay: You cannot afford to repay a loan in 2 weeks but can handle $100–$300/month for 12–24 months.

- Lower total cost: Even at 36% APR, an installment loan costs far less than a 391% APR payday loan over the same period.

Real-World Cost Example

Let us compare the total cost of borrowing $1,000 for 30 days:

- Payday loan (391% APR): $1,000 principal + $320 fee = $1,320 total. If you cannot repay and roll over once, the total becomes $1,640.

- Installment loan (24% APR): $1,000 principal + $20 interest for 30 days = $1,020 total. Over 12 months, the total cost is approximately $1,134.

The payday loan costs 16x more than the installment loan for the same 30-day period. Over a year, the difference is even more dramatic — a rolled-over payday loan can cost $4,000+ on a $1,000 principal.

Bad-Credit Options for Both

If your credit score is below 580, you still have options for both loan types:

- Bad-credit payday loans: Higher fees (up to $30/$100), shorter terms, and more aggressive collection practices. Only borrow if you are 100% certain you can repay on time.

- Bad-credit installment loans: Online lenders (Upstart, Avant, OneMain) and credit unions offer installment loans for scores as low as 500. APRs range from 25–36%. You may need a co-signer or collateral.

Credit unions are the best option for bad-credit installment loans. Many offer "credit builder" loans designed specifically to help you establish payment history. APRs are typically 8–18%.

Alternatives to Both

Before choosing either loan type, consider these alternatives that may be cheaper or safer:

- Cash advance apps (Dave, Earnin, Brigit): $0–$10/month membership, no interest, no credit check. Best for small amounts ($50–$500).

- Credit union Payday Alternative Loans (PALs): APR capped at 28%, 1–6 month terms. Available even to members with poor credit.

- Employer paycheck advances: Some employers offer early wage access with zero fees. Ask your HR department.

- Negotiate with creditors: Call the company you owe and ask for a payment plan or extension. Most prefer to work with you rather than send the debt to collections.

- Community assistance: Nonprofit organizations and 211 hotlines offer emergency grants, food assistance, and utility relief.

Bottom Line

Installment loans are almost always the better choice for amounts over $500 or when you need more than 2 weeks to repay. The lower APR, fixed payments, and credit-building benefits make them a smarter financial tool. Payday loans should be a last resort for true emergencies under $500 that you can repay in full on your next payday.

Before borrowing, calculate the total cost of each option including fees and interest. If the total cost exceeds your ability to repay, do not borrow — seek alternatives instead.

Disclosure: CashAdvanceFinder.com is not a financial advisor. This content is for educational purposes only and does not constitute professional advice. Always compare APRs, fees, and terms from multiple lenders before borrowing.