When you are short on cash before payday, two options come up most often: a traditional payday loan or a cash advance app. Both promise fast money, but they work very differently — and the difference in cost can be hundreds of dollars. This guide breaks down exactly what sets them apart so you can make an informed decision.

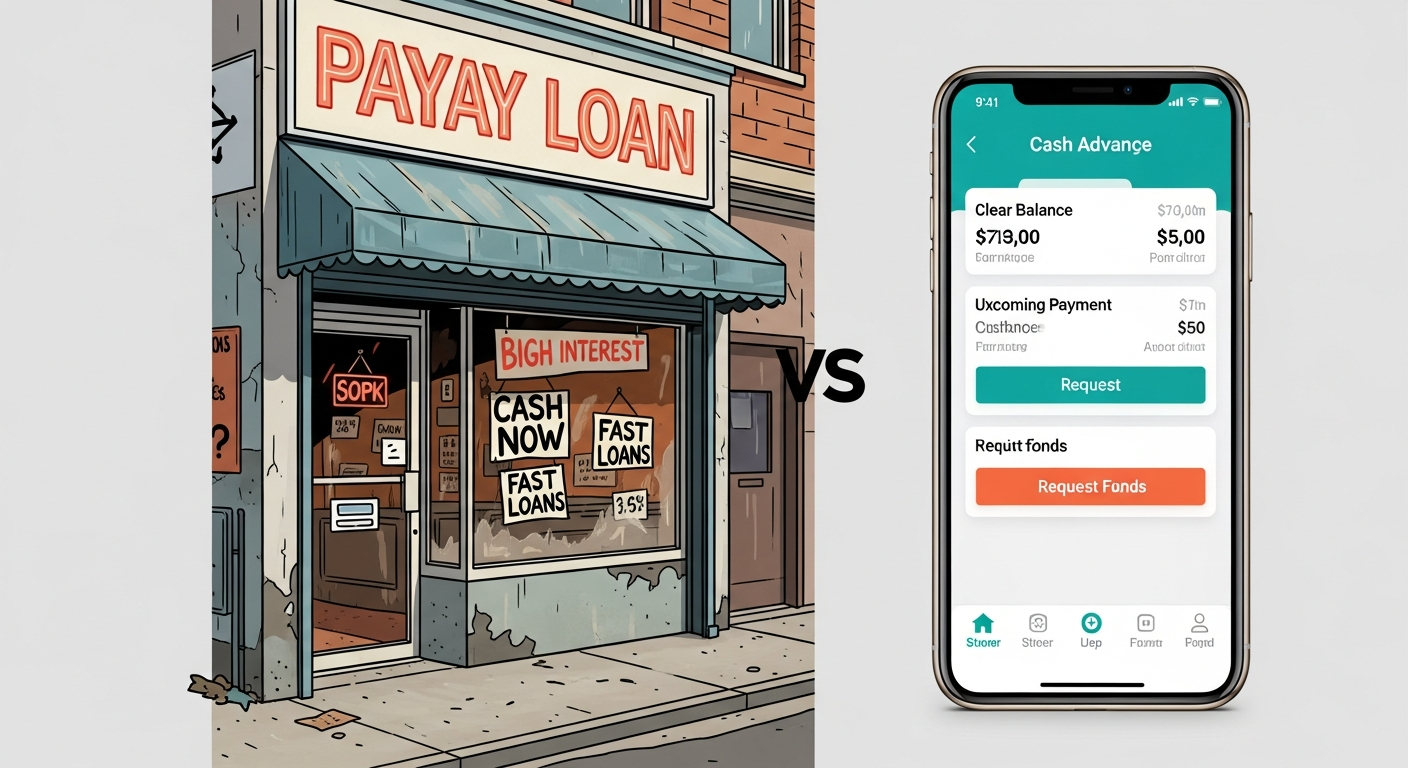

What Is a Payday Loan?

A payday loan is a short-term, high-cost loan typically ranging from $100 to $1,000. You borrow money today and repay the full amount — plus a fee — on your next payday. Payday loans are offered by storefront lenders, online lending platforms, and some check-cashing outlets.

The defining characteristic of payday loans is their cost. Lenders typically charge $10–$30 per $100 borrowed. That sounds modest, but when expressed as an Annual Percentage Rate (APR), a typical two-week payday loan carries an APR between 300% and 400%. On a $300 loan, you might repay $345 two weeks later — a $45 fee that adds up fast if you roll the loan over.

Most payday lenders do not perform a traditional hard credit check, but they may verify your identity, income, and bank account information through alternative data.

What Is a Cash Advance App?

A cash advance app (also called an earned wage access app) connects directly to your bank account and advances you a portion of your upcoming paycheck — usually $50–$750. The advance is repaid automatically when your next direct deposit arrives.

Unlike payday loans, most cash advance apps charge no interest. They generate revenue through optional tips (Earnin), small monthly membership fees ($1/month for Dave, $9.99/month for Brigit), or optional instant-funding fees ($1.99–$8.99 per transfer). These costs are significantly lower than payday loan fees in nearly every scenario.

Head-to-Head Comparison

| Category | Payday Loan | Cash Advance App |

|---|---|---|

| Typical APR | 300%–400% | 0% (fees only) |

| Max amount | $100–$1,000+ | $50–$750 |

| Repayment | Lump sum on payday | Auto-debit on payday |

| Hard credit check | Sometimes | Rarely/never |

| Speed | Same day | Instant to 5 days |

| Rollover risk | High | Low (no rollover) |

| State regulations | Heavily regulated | Lighter regulation |

The Real Cost Difference

Let's compare borrowing $300 until payday (two weeks away):

- Payday loan at $15 per $100: You repay $345 — a $45 fee. APR: ~391%.

- Dave ($1/month + $5 express fee): Total cost to borrow $300 instantly: ~$6 for the month. APR equivalent: about 52% — but you are paying a flat fee, not interest.

- Earnin (no fee, voluntary tip): If you tip $3, the full cost is $3. If you tip nothing, it's free.

The savings are substantial. For someone who borrows $300 twice a month using a payday loan, the annual fee cost could exceed $1,080. With an app, the same behavior might cost $12–$24/year in membership fees.

When a Payday Loan Might Make More Sense

Despite higher costs, payday loans are sometimes the only option in certain situations:

- You need more than $750 — which exceeds most cash advance app limits.

- Your bank account is too new or irregular for apps to verify income.

- You are paid in cash or don't have regular direct deposits.

- You need funds immediately in cash (some payday lenders offer cash in hand).

In these cases, compare multiple lenders carefully. Look for the lowest APR, read the full repayment terms, and confirm whether the lender reports to credit bureaus.

The Debt Cycle Risk

The biggest danger with payday loans is the rollover trap. If you cannot repay the full loan on payday, many lenders allow you to "roll over" the loan — extending it for another two weeks and paying another fee. This can quickly snowball: a $300 loan can grow to $450 or more within six weeks if you keep rolling it over.

Cash advance apps eliminate this risk by design. They simply withdraw what they advanced — no more. If your bank account doesn't have enough funds, the app may delay the collection or contact you, but there is no accumulating interest or penalty fees in most cases.

Bottom Line

For most borrowers, cash advance apps are the smarter, safer, and significantly cheaper option for small short-term needs under $750. Payday loans should be a last resort, used only when app-based advances are not available and you have a clear repayment plan.

Whichever route you take, borrow only what you can confidently repay on your next payday. Short-term borrowing tools are not designed for recurring financial shortfalls — if you find yourself relying on them every month, that is a signal to revisit your budget.

Disclosure: CashAdvanceFinder.com is not a lender and does not originate loans. This article is for informational purposes only.