When you need to borrow money and have limited options, two products dominate the short-term lending space: installment loans and payday loans. They are often grouped together, but they are fundamentally different in cost, structure, and long-term impact. Understanding the difference can save you hundreds of dollars and prevent a debt spiral.

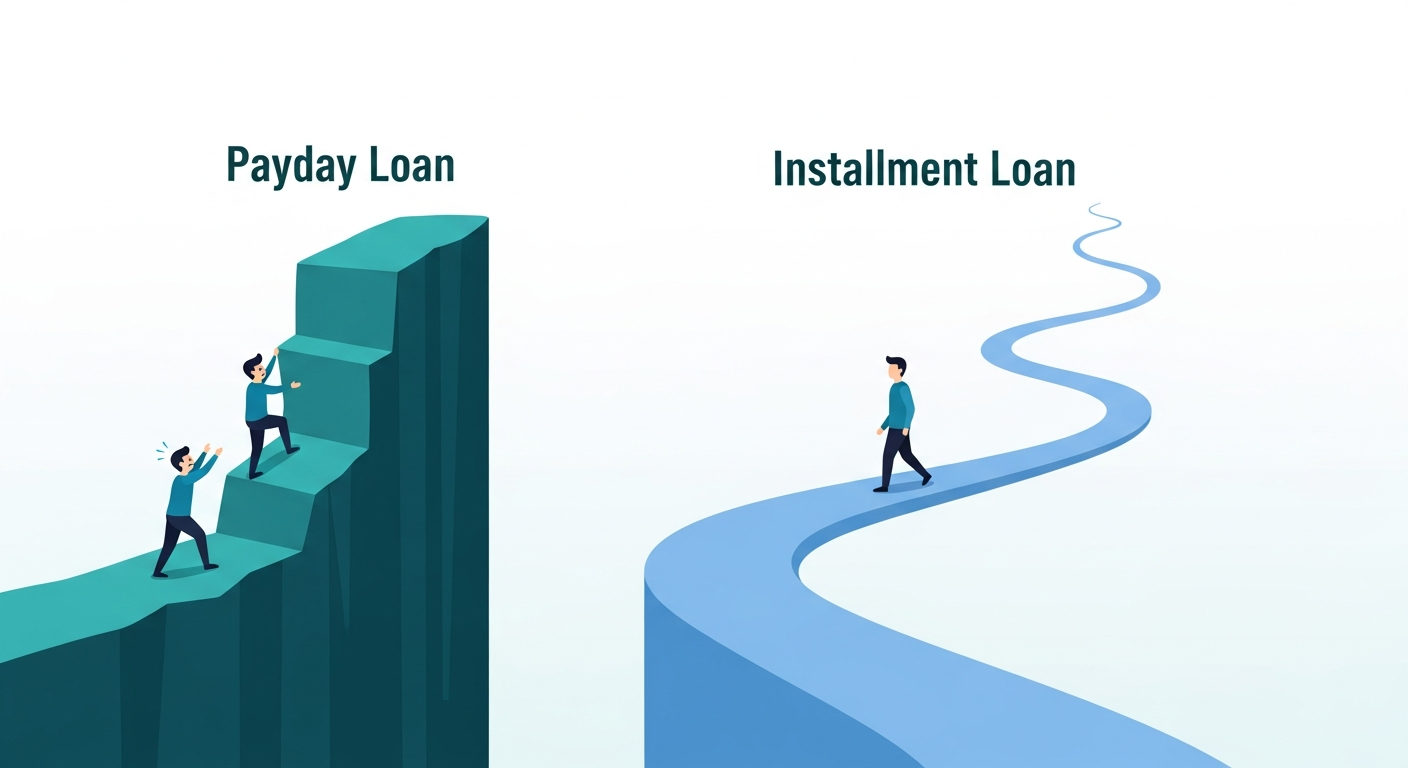

What Is a Payday Loan?

A payday loan is a short-term loan, typically $100–$1,000, due in full on your next payday (usually 14–30 days). The fee is typically $10–$30 per $100 borrowed, which translates to an APR of 300%–400%. The full repayment is a single lump sum — principal plus fee — withdrawn from your bank account on the due date.

Key characteristic: Repayment is a single lump sum. If you cannot repay, you can "roll over" the loan for another fee, which is how the debt cycle begins.

What Is an Installment Loan?

An installment loan is also a short-term loan, typically $500–$5,000, but repaid over multiple months — usually 3 to 12 months. Each payment includes a portion of the principal plus interest. The APR is typically lower than payday loans, ranging from 25% to 300%, depending on the lender, state, and your credit profile.

Key characteristic: Repayment is spread over multiple payments. There is no single lump sum due on payday, and the repayment structure is predictable.

Side-by-Side Comparison

| Feature | Payday Loan | Installment Loan |

|---|---|---|

| Loan amount | $100–$1,000 | $500–$5,000 |

| Repayment term | 2–4 weeks | 3–12 months |

| APR | 300%–400% | 25%–300% |

| Payment structure | Single lump sum | Monthly payments |

| Rollover risk | High | Low |

| Credit check | Soft or none | Soft or hard |

| Credit reporting | Rarely | Often |

| State regulation | Heavily regulated | Less regulated |

The Real Cost: A $1,000 Example

Let's compare borrowing $1,000 in a typical scenario:

- Payday loan: $1,000 with $25 per $100 fee = $250 fee. Total due in 2 weeks: $1,250. APR: ~325%. If you roll over once, you owe another $250. Total cost in 1 month: $500.

- Installment loan: $1,000 at 99% APR for 6 months. Monthly payment: ~$198. Total paid: ~$1,188. Total interest: $188.

The installment loan costs significantly less — $188 vs. $500 or more — and the payments are spread out, making it easier to manage without falling into a cycle.

When Installment Loans Are Better

- You need $500 or more.

- You cannot afford a single lump-sum repayment on your next payday.

- You want a predictable monthly payment.

- You want to avoid the rollover trap.

- You want the loan to be reported to credit bureaus (installment loans often report to all three bureaus, which can help build credit if you pay on time).

When Payday Loans Might Make Sense

- You need less than $500 and can repay the full amount on your next payday.

- You need the money today and don't qualify for an installment loan (very bad credit or no credit).

- You need cash in hand (some payday lenders offer cash).

Even then, a cash advance app is often a better alternative for amounts under $750.

Where to Find Legitimate Installment Loans

Online lenders like OppLoans, RISE, and OneMain Financial offer installment loans to borrowers with credit scores as low as 300. APRs are typically 59%–199%, which is high but still lower than payday loans. Credit unions and some community banks also offer short-term installment loans with APRs below 28%.

Bottom Line

Installment loans are almost always the better choice over payday loans for amounts over $500. The lower effective APR, predictable monthly payments, and absence of the rollover trap make them significantly safer. If you need less than $500, consider cash advance apps before either option. If you choose a payday loan, treat it as a one-time solution, not a habit — and only borrow what you can repay on your next payday.

Disclosure: CashAdvanceFinder.com is not a lender and does not make credit decisions. This content is for informational purposes only.